Turtlemint’s Market Debut: A Strategic Milestone for India’s Insurtech Ecosystem

As the Indian stock markets prepare for the listing of insurtech major Turtlemint on Monday, June 29, the financial ecosystem is abuzz with the implications of the company’s recent initial public offering (IPO). With a 1.2X oversubscription rate, the IPO signals sustained investor appetite for digital-first insurance distribution platforms, even as the company navigates the challenges of a scaling, loss-making enterprise.

The public issue, which saw a price band of ₹144–₹152 per share, effectively valued the company at approximately ₹4,513 Cr ($475 Mn). Beyond the capital raised, the IPO served as a liquidity event for some of the most influential venture capital firms in the country, highlighting the success of the long-term bets placed on India’s fintech growth story.

Main Facts: The Anatomy of the IPO

Turtlemint’s IPO was structured as a dual-pronged financial instrument: a fresh issue of shares totaling ₹660.7 Cr and an Offer for Sale (OFS) of 1.46 Cr shares by existing promoters and institutional backers.

The primary objective of the fresh capital is to fuel the company’s aggressive growth strategy. Management has indicated that proceeds will be directed toward bolstering technology infrastructure, enhancing product development, intensifying marketing efforts, meeting working capital requirements, and exploring potential inorganic growth through strategic acquisitions.

The IPO’s success was further bolstered by a robust anchor round. Prior to the public opening, Turtlemint secured ₹397.2 Cr by allotting 2.61 Cr equity shares to institutional giants, including seven domestic mutual funds managing 12 distinct schemes. International entities such as Societe Generale, 360 One, Amansa Holdings, BNP Paribas, and Citi Group also participated, signaling strong confidence from the global institutional community.

Chronology: From Private Backing to Public Markets

The journey to the bourses has been a decade-long evolution for the company, founded in 2015 by Anand Prabhudesai and Dhirendra Nalin Mahyavanshi.

- 2015: Turtlemint is founded with the mission to bridge the gap between complex insurance products and the average Indian consumer through a digital-first, advisor-led model.

- Early Growth Years: The company builds a robust network of financial advisors, enabling the distribution of car, bike, health, and term life insurance policies, effectively digitizing the traditional agency model.

- Pre-IPO Scaling: Throughout the 2020s, the company focuses on hyper-growth, expanding its reach across Tier-II and Tier-III cities, while simultaneously absorbing the high customer acquisition costs typical of the insurtech sector.

- Early 2026: Turtlemint files its updated Draft Red Herring Prospectus (DRHP), outlining the intent to raise ₹660.7 Cr.

- Mid-2026 (June): The IPO opens, attracts significant anchor interest, and closes with a 1.2X oversubscription.

- June 29, 2026: The official listing on the bourses marks the company’s transition into a publicly traded entity.

Supporting Data: Investor Gains and Shareholder Exit Patterns

The IPO provided a significant exit window for venture capital firms that have supported Turtlemint since its early days. The returns generated underscore the high-risk, high-reward nature of the insurtech sector.

The Big Winners

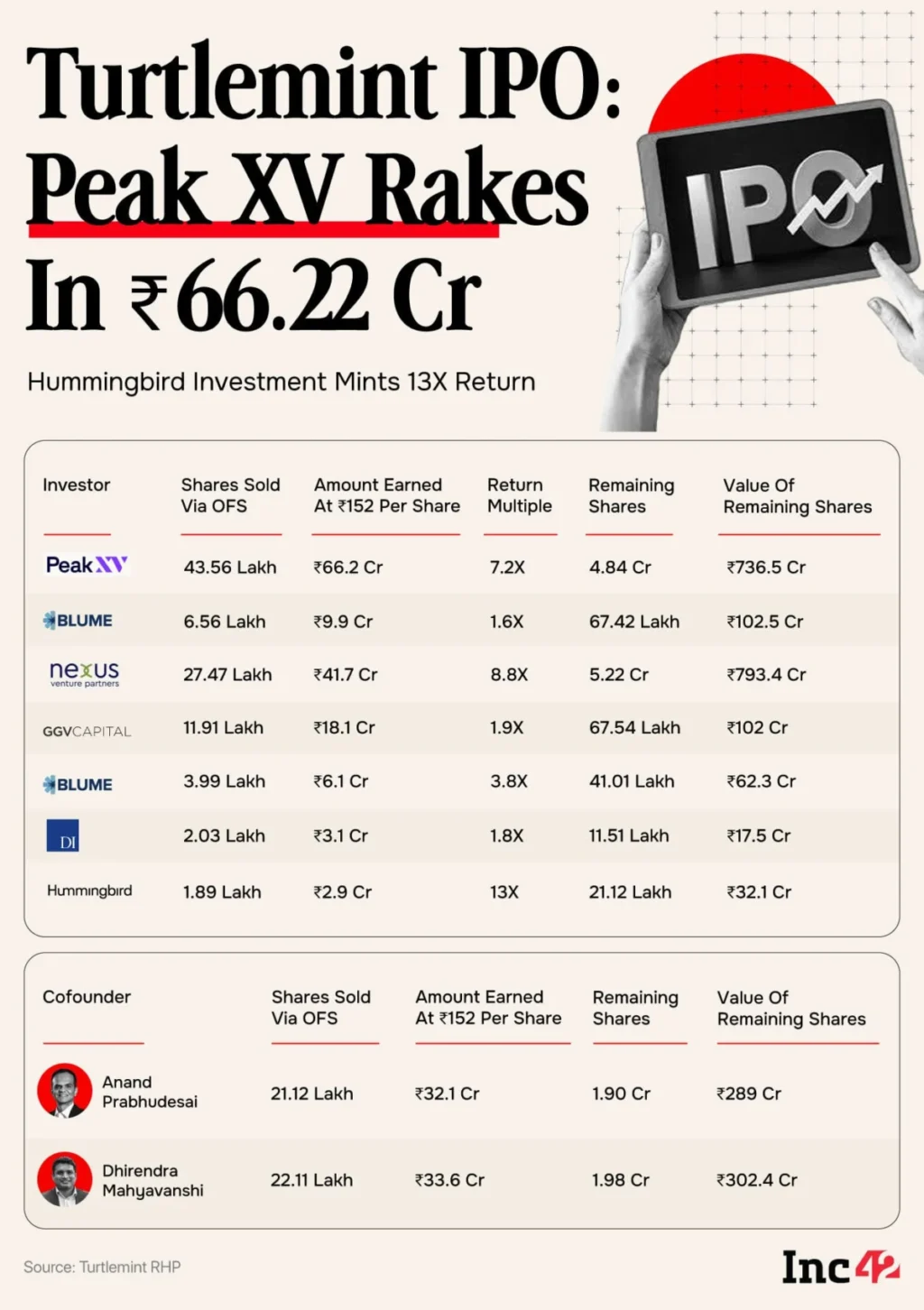

The most notable performance came from Hummingbird Ventures, which realized a 13X return on its initial investment. The firm sold 1.89 Lakh shares, netting ₹2.9 Cr, while maintaining a substantial residual holding of 21.12 Lakh shares valued at ₹32.1 Cr.

Nexus Venture Partners, one of the earliest institutional backers, also saw strong results. By offloading 27.47 Lakh shares for ₹41.75 Cr, the firm booked an 8.8X return. Crucially, Nexus remains the largest selling shareholder, with a remaining stake of 5.22 Cr shares valued at ₹793.4 Cr, signaling continued long-term faith in the platform.

Peak XV Partners, one of the company’s largest stakeholders, offloaded 43.56 Lakh shares at the issue price of ₹152, resulting in a ₹66.2 Cr payout. This represents a 7.2X return on their initial investment. Following the sale, Peak XV retains 4.84 Cr shares worth ₹736.5 Cr.

Other Notable Participants

- Blume Ventures: Through two of its funds, Blume secured a combined ₹16.5 Cr. While Fund 1X recorded a 1.6X return, the Opportunities Fund IIA achieved a 3.8X return. They retain a significant holding of 1.08 Cr shares.

- GGV Capital: Recorded a 1.9X gain by selling 11.91 Lakh shares for ₹18.11 Cr.

- Dream Incubator: The Japanese firm exited a portion of its holding, booking a 1.8X return on the sale of 2.03 Lakh shares.

The Founders’ Stake

Co-founders Anand Prabhudesai and Dhirendra Nalin Mahyavanshi participated in the liquidity event as well. Combined, they cashed out ₹65 Cr.

- Prabhudesai: Sold 21.12 Lakh shares for ₹32.1 Cr; he retains 1.9 Cr shares valued at ₹289 Cr.

- Mahyavanshi: Sold 22.11 Lakh shares for ₹33.6 Cr; he retains 1.98 Cr shares valued at ₹302.4 Cr.

Official Responses and Financial Standing

While the investor exits paint a picture of success, the financial metrics released in the lead-up to the IPO reveal a company in a state of rapid, albeit costly, expansion.

For the first nine months (9M) of FY26, Turtlemint reported a revenue of ₹741.1 Cr, a staggering 80% increase from the ₹411.1 Cr reported in the same period in FY25. However, this growth has come at the expense of profitability. The company’s net loss widened to ₹187.3 Cr in 9M FY26, a 20% increase from the ₹154.7 Cr loss in the corresponding period of the previous year.

Management has remained transparent about these figures, attributing the losses to the heavy investments required to scale the digital infrastructure and expand the advisor network. The leadership maintains that the path to profitability lies in operational leverage—as the platform processes a higher volume of insurance policies, the marginal cost of distribution is expected to decrease.

Implications: The Road Ahead for Insurtech

The listing of Turtlemint is a litmus test for the broader Indian insurtech landscape. Several critical implications arise from this market entry:

1. Market Validation of the Advisor Model

Turtlemint’s success in growing its revenue base proves that the "phygital" model—combining digital efficiency with human advisory—remains the gold standard for insurance penetration in India. By empowering local agents with technology, Turtlemint has effectively tapped into the trust-based economy of insurance, a model that purely digital players have often struggled to replicate.

2. The Pressure of Public Markets

As a private entity, Turtlemint was judged by growth metrics and investor sentiment. As a public company, the scrutiny will intensify. The 20% rise in net losses year-on-year is a metric that institutional investors will watch closely in the coming quarters. The company will be under immense pressure to demonstrate a concrete roadmap toward narrowing these losses while sustaining its revenue momentum.

3. Consolidation Potential

With a fresh infusion of capital earmarked for "inorganic growth," the market should anticipate consolidation. Turtlemint is well-positioned to acquire smaller, niche insurtech players or regional distributors to strengthen its moat. The IPO provides the company with the currency (both in cash and valuation) to execute these M&A deals, potentially reshaping the competitive landscape.

4. A Template for Future IPOs

The structure of this IPO—specifically the heavy participation of anchor investors and the controlled exit of early-stage VCs—provides a template for other late-stage fintech startups. By balancing the need for liquidity for early backers with the requirement for long-term growth capital, Turtlemint has demonstrated how to navigate the current IPO environment successfully.

Conclusion

As Turtlemint transitions into the public domain, it carries the weight of high expectations. The significant gains booked by early investors like Nexus and Peak XV serve as a testament to the platform’s value creation over the last decade. However, the real work begins now. To maintain investor confidence, the company must successfully pivot from its current "growth-at-all-costs" phase to a model that balances aggressive expansion with sustainable financial health. Monday’s listing will be the first of many chapters in this new phase of the company’s evolution, and all eyes in the financial district will be on its performance in the weeks to follow.