The Indian Fintech Renaissance: A June of Mega-Deals, Strategic Pivots, and Regulatory Evolution

The month of June has served as a defining chapter for the Indian fintech ecosystem, characterized by massive capital inflows, high-profile leadership transitions, and a rigorous recalibration of the regulatory landscape. As the sector matures from a "growth-at-all-costs" phase into a sustainable, compliant, and deeply integrated financial backbone for the nation, the events of the past thirty days have set the tone for the remainder of the fiscal year.

The Headline Movements: A Shifting Power Dynamic

The most significant tremor in the market was the announcement that CRED had secured a massive $900 million (₹8,550 Cr) in a Series H funding round led by Meta. This valuation, placing the post-money worth of the company at $4.5 billion, underscores the enduring confidence investors place in high-engagement consumer fintech platforms.

However, the fiscal news was eclipsed by the strategic narrative surrounding the deal: Kunal Shah, the founder of CRED, has stepped away from his day-to-day operations to assume the role of Global Head of WhatsApp at Meta. This "watershed moment" signals a potential deeper integration between Meta’s communication infrastructure and India’s financial services ecosystem, a move that could redefine how digital payments and credit are distributed across the country.

Simultaneously, the IPO pipeline continues to thicken. Razorpay, the payment gateway giant, has filed confidential draft papers with SEBI, aiming to raise between ₹5,000 and ₹6,000 Cr. Not far behind, Sachin Bansal’s Navi is currently in advanced discussions to raise $250–300 million to fortify its lending book ahead of its own anticipated public listing. On the retail front, Turtlemint’s recent public issue of ₹882.67 Cr closed with a 1.2X oversubscription—a modest but significant achievement that highlights a cautious yet receptive public market.

The Regulatory Tightening: A New Era of Compliance

While the funding news captures headlines, the structural changes occurring in the background are arguably more transformative. The Reserve Bank of India (RBI) and the Insurance Regulatory and Development Authority of India (IRDAI) are moving toward a more guarded, consumer-protective stance.

Payment platforms are currently deep in the process of calibrating their compliance stacks to accommodate a proposed one-hour cooling-off window for UPI and IMPS transfers exceeding ₹10,000. This measure is a direct response to the rising tide of sophisticated digital fraud. Furthermore, the RBI is actively advancing two "kill-switch" initiatives, designed to provide a centralized mechanism to halt fraudulent transactions instantly across the financial ecosystem, effectively empowering the regulator to protect the integrity of the digital economy in real-time.

Insurance remains another hotbed of regulatory activity. The IRDAI has proposed stringent disclosure norms for insurance intermediaries, forcing a higher degree of transparency regarding commission structures. For distribution-heavy insurtechs and digital broking platforms, this represents a major operational shift, potentially compressing margins but ultimately cleaning up the ecosystem of mis-sold products.

Spotlight: Five Fintech Startups to Watch

Against this complex backdrop of rapid growth and tightening oversight, Inc42 has identified five startups that are navigating the changing currents with agility and innovation.

1. Blostem: Democratizing Banking Infrastructure

The integration bottleneck is a perennial problem for Indian fintech. Offering fixed deposits (FDs) traditionally requires months of individual bank integrations. Delhi-based Blostem, founded in 2021 by Sandeep Garg, Ravi Jain, Uday Sharma, and Pankaj Pratap Singh, has solved this with a single, plug-and-play API layer.

- The Model: By integrating once, platforms gain access to a network of 10 banks and NBFCs, including Suryoday SFB and Bajaj Finance.

- The Impact: With backing from Zerodha’s Rainmatter and AC Ventures, Blostem is positioning itself to capture 40% of India’s digital FD volumes by lowering the barrier to entry for wealthtech and payment apps.

2. Finanjo: The Behavioral Edge

Most personal finance apps suffer from high churn because they offer static data that users find guilt-inducing rather than helpful. Jaipur-based Finanjo, founded in 2025 by Prithviraj and Pankaj Singh Chauhan, flips the script.

- The Model: Its AI assistant, "Jo," doesn’t just track expenses; it provides actionable, behavioral-based guidance.

- The Impact: With 5,000 users and ₹25 Cr in connected savings in its beta phase, Finanjo is proving that users are looking for a financial mentor rather than just a digital ledger.

3. Finfinity: Buyer-Centric Lending

In a market saturated with loan aggregators that prioritize lender commissions, Mumbai-based Finfinity is focusing on the borrower. Founded in 2023, the platform offers a transparent, buyer-centric marketplace for home, personal, and auto loans.

- The Model: Using deep-tech integrations for live data exchange, Finfinity provides real-time, personalized loan recommendations based on the borrower’s profile, not the lender’s incentive.

- The Impact: Backed by the Mankind Pharma promoter’s family office, the startup is aiming for a 10 million user base within the next two years, leveraging its partnerships with major institutions like IDFC First and Muthoot Finance.

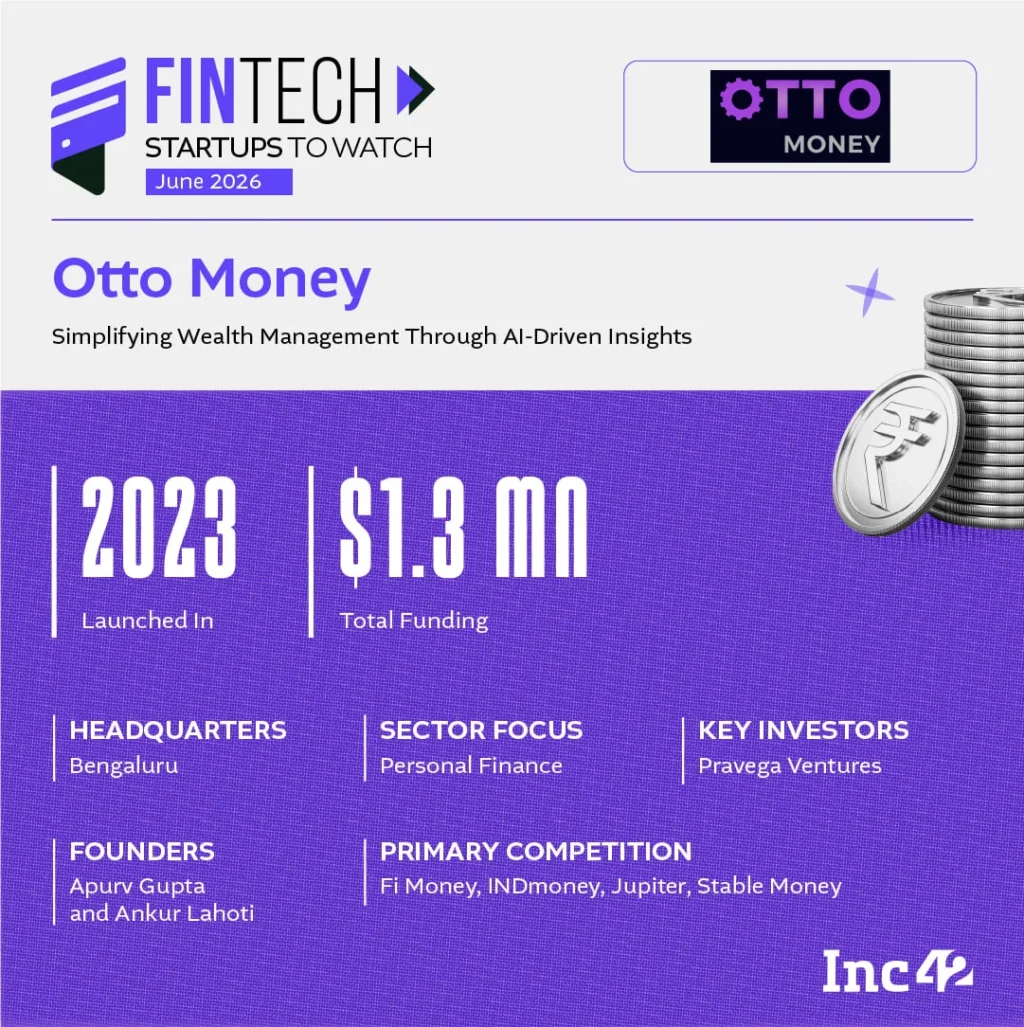

4. Otto Money: Unbiased Wealth Guidance

Wealth management in India has long been hampered by the conflict of interest inherent in commission-based product distribution. Otto Money, a Bengaluru-based startup founded in 2025, is a "pure-play" wealth guidance platform that abstains from product distribution.

- The Model: Otto uses institution-grade AI models to provide multi-asset portfolio guidance, explaining risk trade-offs without the pressure to sell specific financial products.

- The Impact: Having raised $1.3 million from Pravega Ventures, Otto is catering to a new generation of sophisticated retail investors who demand analytical clarity over product pitches.

5. FatakPay: Financial Wellness for Bharat

Access to formal credit remains a challenge for over 450 million Indians who are "invisible" to traditional, salary-based underwriting systems. FatakPay, founded by Amit Lodha, Amit Goyal, Ajit Kumar, and Abhishek Gandhi, is bridging this gap.

- The Model: Operating as a full-stack financial wellness app, it offers instant, collateral-free loans, CIBIL monitoring, and micro-investment options.

- The Impact: With over 20 million users and ₹2,500 Cr in total disbursements, FatakPay is moving beyond lending with products like "FatakUdaan" and "FatakSecure," aiming to provide a comprehensive financial safety net for gig workers and blue-collar employees in Tier II and III cities.

Implications and Future Outlook

The trajectory of the Indian fintech sector in June reveals a fundamental shift: the market is moving toward utility and trust.

The massive funding for players like CRED suggests that consumer engagement remains the primary metric for valuation, but the regulatory focus from the RBI and IRDAI suggests that the "Wild West" days of fintech are ending. Startups that prioritize transparent infrastructure (like Blostem), unbiased guidance (like Otto Money), and inclusion (like FatakPay) are likely to be the long-term winners.

As Razorpay and potentially other giants prepare for the public markets, the focus will increasingly shift to profitability and regulatory resilience. For the startups highlighted above, the challenge will be to maintain their hyper-growth trajectories while adhering to the increasingly stringent standards of the Indian financial ecosystem. One thing is certain: as the digital financial infrastructure of India becomes more robust, the competitive landscape will favor those who provide genuine value rather than those who simply facilitate transactions.