The Great Indian Tech IPO Surge: Mapping the Evolution of a $143 Billion Ecosystem

For years, the Indian startup ecosystem was viewed through the lens of potential—a landscape defined by ambitious founders, venture capital infusions, and a relentless pursuit of scale. Today, that "kid" has grown into a formidable adult. The most telling indicator of this maturation is not just the volume of funding, but the migration from private boardrooms to the public bourses.

A public listing has long been the gold standard for Indian enterprise, symbolizing transparency, operational maturity, and long-term viability. For the new-age tech sector, the Initial Public Offering (IPO) has evolved from a distant ambition into a critical rite of passage. It serves as the ultimate validation of a business model, providing a definitive pathway for early investors to realize exits while unlocking immense wealth for founders and employees.

As of mid-2026, the transformation is undeniable. With over 60 new-age tech companies now trading on Indian exchanges and international platforms like Nasdaq, the "IPO wave" is no longer a trend—it is the new normal.

The Velocity of Public Debuts: A Chronological Shift

The momentum behind this shift reached a crescendo in 2025, a year that will be remembered as the tipping point for the Indian startup IPO story. While 2024 saw a respectable 13 startups make their market debut, 2025 shattered expectations with 18 companies ringing the opening bell.

The 2025 cohort was characterized by household names and sector leaders, including Meesho, Ather Energy, Urban Company, Lenskart, Groww, Pine Labs, and PhysicsWallah. This surge demonstrated that investors were no longer wary of tech-heavy balance sheets, provided there was a clear, actionable path to profitability.

The momentum has carried forward into 2026. In the first half of the year alone, six major players—Kissht, Aye Finance, Fractal Analytics, Amagi, Shadowfax, and SEDEMAC—have successfully transitioned to the public markets. This sustained cadence confirms that the pipeline remains robust, with roughly 15 other high-profile startups, including Zepto, Shiprocket, and OYO, currently navigating the various stages of their own IPO journeys.

The "Profitability First" Mandate

Historically, Indian startups were stigmatized as "cash-burning machines," prioritizing customer acquisition and market share over the bottom line. This growth-at-all-costs philosophy defined the funding boom of 2020-22. However, the onset of the funding winter in 2022 served as a brutal, necessary reality check.

The current landscape is defined by a pivot toward fiscal discipline. Data reveals that 64% of listed new-age tech companies are now operating in the green. This shift was not merely a reaction to market pressure; it was a prerequisite for IPO success. Institutional investors, burnt by past volatility, now demand a clear trajectory toward sustainable earnings.

Profitability Leaders

The financial landscape is anchored by stalwarts who have proven that scale and profit can coexist. Info Edge, led by Sanjeev Bikhchandani, remains the gold standard, reporting a net profit of ₹962 Cr in FY25. Other long-term players like Justdial (₹584 Cr) and IndiaMART (₹551 Cr) continue to underscore the long-term viability of the consumer services and B2B ecommerce models.

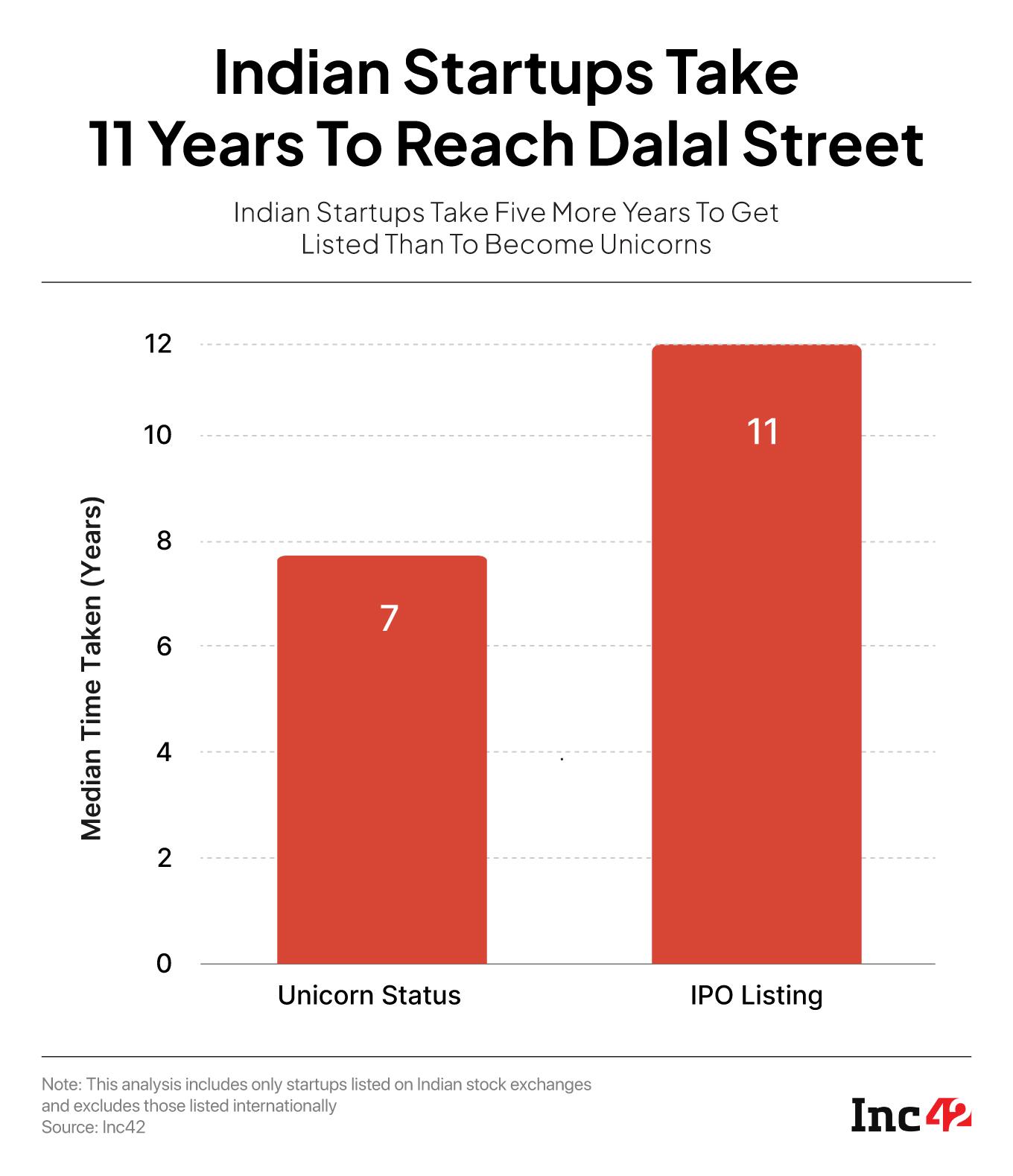

However, the path to the bourses is not uniform. While the median time for a startup to reach an IPO is roughly 11 years, the ecosystem is witnessing outliers. Companies like ArisInfra have managed to hit the public markets in just four years, while veterans like ixigo took nearly two decades to make the leap.

Sectoral Dominance: Fintech, Ecommerce, and Enterprise Tech

The composition of the public markets mirrors the broader investment trends of the past decade. The sectors that attracted the most private capital—Fintech, Ecommerce, and Enterprise Tech—now dominate the stock exchange listings.

- Fintech & Enterprise Tech: These sectors lead the pack with 12 listings each. The integration of financial services into daily digital habits and the global demand for Indian SaaS (Software as a Service) have created strong value propositions for public investors.

- Ecommerce: With 11 listings, the ecommerce sector remains a pillar of the digital economy. While volatility has plagued some, others have successfully built defensible moats.

The future of these sectors looks even more crowded. As giants like PhonePe, Zepto, and OYO prepare for their eventual public entries, the sectoral weight of tech on the NSE and BSE will only intensify. Furthermore, the real-estate tech space is seeing renewed interest, with the anticipated entry of firms like Infra.Market, which has already filed its papers confidentially with the SEBI.

Geography of Wealth: The Rise of Delhi NCR

While Bengaluru is traditionally hailed as the startup capital of India, the "IPO race" tells a different story. Delhi NCR (encompassing Delhi, Gurugram, and Noida) has emerged as the clear leader in producing listed tech entities.

With 25 listed companies calling the region home, Delhi NCR significantly outpaces Bengaluru (17) and Mumbai (11). Gurugram acts as a magnet for logistics and travel-tech giants like Delhivery and Lenskart, while Noida hosts fintech powerhouses like Paytm. The economic impact is profound: Delhi NCR alone contributes $77.8 billion to the cumulative $143 billion market capitalization of listed new-age tech companies.

Implications: A New Maturity for the Indian Economy

The transition of 60+ startups into public entities has profound implications for the Indian financial ecosystem.

1. Increased Transparency and Governance

Public listing mandates a level of corporate governance that private startups often bypass. This shift is forcing a higher standard of reporting, auditing, and board-level accountability across the sector.

2. The Wealth Multiplier Effect

The IPO surge is creating a new class of wealth in India. Beyond the founders, the liquidity provided to early employees and institutional investors is being recycled back into the ecosystem, fueling the next generation of early-stage ventures.

3. Investor Confidence

The volatility of stocks like Paytm or Fino Payments Bank serves as a cautionary tale, yet the massive success of companies like E2E Networks—which has seen a 7030% growth in market cap since its listing—provides the upside that keeps the market hungry. Investors are becoming more sophisticated, learning to distinguish between "growth-at-all-costs" and "sustainable scaling."

4. Regulatory Evolution

The SEBI’s evolving framework for IPOs, including the allowance for confidential filings, has streamlined the process for tech companies. This regulatory support is crucial for ensuring that India remains a competitive destination for both domestic and international capital.

Conclusion: The Path Ahead

The Indian tech IPO story is no longer about the novelty of a startup going public; it is about the integration of these entities into the bedrock of the national economy. With a combined market capitalization of over $143 billion, these companies are no longer just "startups"—they are the blue-chip companies of tomorrow.

As the "Indian Listed New-Age Tech Company Tracker" continues to update, the focus for the next 18 months will be on consolidation. Can those currently in the red turn the corner? Will the next cohort of IPOs maintain the valuation premiums seen in the 2025 boom?

The answers to these questions will define the next chapter of India’s economic narrative. One thing is certain: the era of the "unlisted startup" as the dominant form of enterprise is waning, replaced by a more mature, transparent, and public-facing digital economy. The Dalal Street ride for Indian startups has only just begun.

Source: Inc42 Analysis, Public Market Data. Updated as of June 13, 2026.