Global Smart Wearable Market Maintains Upward Momentum: Q1 2026 Analysis

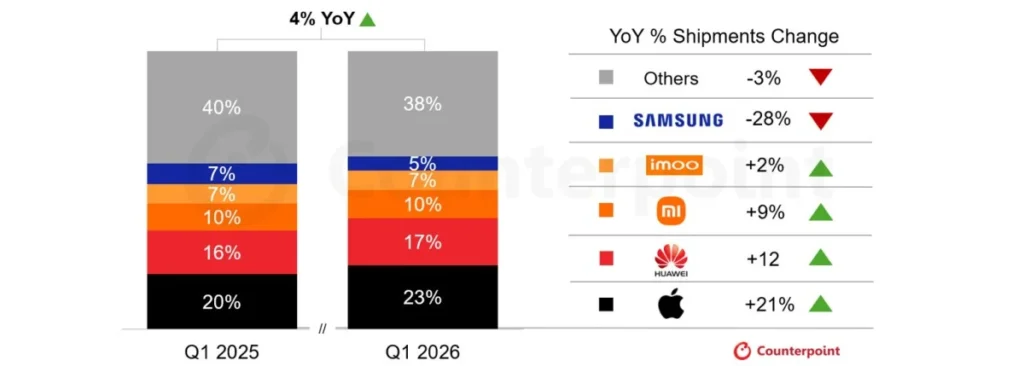

The global smart wearable market has officially entered a period of sustained revitalization. According to the latest comprehensive report from Counterpoint Research, the industry witnessed a 4% year-over-year (YoY) growth in the first quarter of 2026. This performance marks a critical juncture for the sector, signaling a definitive recovery from the market turbulence that characterized the 2024 fiscal year and building upon the tentative stabilization observed throughout 2025.

As consumer sentiment shifts toward high-end technology, the wearable landscape is being redefined by premiumization. Analysts note that manufacturers are increasingly prioritizing advanced sensor integration and sophisticated health-tracking suites to meet the demands of a more discerning global audience.

Main Facts: A Resurgent Market

The data for Q1 2026 highlights a significant shift in consumer purchasing behavior. While the overall volume of shipments grew by a modest 4%, the value of the market has surged more aggressively. The Average Selling Price (ASP) of smartwatches rose by 6% globally during the first quarter. This discrepancy between volume growth and price growth is the most telling metric of the current cycle: consumers are not merely buying more devices; they are intentionally opting for higher-tier, feature-rich hardware.

Apple continues to dominate the global hierarchy, leveraging its ecosystem lock-in and the successful reception of its latest wearable iterations to maintain a commanding lead. However, the market is far from monolithic. Regional growth patterns, particularly in China, have played an instrumental role in propping up the global numbers, even as traditional stalwarts like Samsung face mounting pressure and declining shipment volumes.

Chronology: The Road to Recovery

To understand the current state of the industry, one must look at the trajectory of the previous 24 months.

2024: The Year of Contraction

The smart wearable market entered 2024 facing a "perfect storm" of economic uncertainty and market saturation. With inflation impacting disposable income in major Western markets and a lack of disruptive innovation in the entry-level segment, global shipments saw a marked decline. Manufacturers struggled with high inventory levels, leading to a year defined by heavy discounting and a temporary cooling of consumer enthusiasm.

2025: The Stabilization Phase

By early 2025, the market began to show signs of life. The excess inventory built up in 2024 had largely been liquidated, allowing manufacturers to reset their supply chains. Throughout the year, companies pivoted their strategy, moving away from "budget-first" devices toward health-centric models that justified higher price tags. By the end of Q4 2025, the industry had successfully pivoted toward a "premium-first" strategy, setting the stage for the growth observed in early 2026.

Q1 2026: The Return to Growth

The first quarter of 2026 serves as the definitive proof of this strategy. With a 4% YoY growth, the industry has successfully exited the recovery phase and entered a period of expansion. The primary drivers have been the rollout of more sophisticated health-tracking sensors, which have transitioned from "luxury features" to "expected baseline requirements" for the average consumer.

Supporting Data: Regional Dominance and Competitive Shifts

The competitive landscape of Q1 2026 reveals a tale of two markets: the established Western stronghold and the hyper-competitive Chinese theater.

The North American Stronghold

North America remains the epicenter of Apple’s dominance. The region accounted for over half of Apple’s total global shipments in Q1 2026. Apple secured the top position globally with a 23% market share, representing an impressive 21% growth compared to Q1 2025. This surge is attributed to the successful adoption of its latest device lineup, which has effectively incentivized existing users to upgrade.

The Chinese Engine

While North America drives value, China is currently driving volume growth. The domestic Chinese market recorded a 15% YoY growth in shipments, a staggering figure compared to global averages. The competitive hierarchy in China is distinct from the rest of the world:

- Huawei: Retains an iron grip on the domestic market with a 40% share. Their ability to integrate proprietary software and high-end hardware has made them virtually untouchable in their home territory.

- Imoo and Xiaomi: These players occupy the second and third positions, respectively, focusing on specific demographics and high-volume, cost-effective devices.

The Samsung Contraction

Not all players are experiencing a renaissance. Samsung, once the primary challenger to Apple’s throne, recorded a significant 28% dip in shipments during Q1 2026. Analysts suggest that Samsung is currently in a "transition period," struggling to balance its high-end Galaxy Watch offerings against the aggressive pricing of Chinese competitors and the aspirational pull of the Apple ecosystem.

Official Responses and Market Analysis

In the wake of the Counterpoint report, industry leaders have been quick to justify these shifts. Representatives from major manufacturers have signaled that the rise in ASP is not merely a pricing strategy, but a reflection of the "value-add" nature of modern wearables.

"Consumers are no longer just looking for a notification mirror for their smartphone," says one industry analyst. "They are looking for clinical-grade health diagnostics—ECG monitoring, blood oxygen tracking, and advanced sleep architecture analysis. The rise in ASP is directly proportional to the R&D costs associated with these technologies."

Conversely, the decline in Samsung’s performance has sparked internal debates regarding the efficacy of its current mid-range strategy. Industry observers note that Samsung’s struggle is a symptom of a "squeezed middle"—where the brand is being undercut by the aggressive innovation of Huawei in the East and the brand-prestige dominance of Apple in the West.

Implications: What to Expect for the Remainder of 2026

The data from Q1 2026 offers a clear roadmap for the remainder of the year. As the market continues to consolidate around premium features, several trends are likely to emerge:

1. The Death of the "Cheap" Smartwatch

As ASPs continue to rise, the entry-level smartwatch market—previously dominated by sub-$50 devices—is expected to shrink further. Manufacturers are increasingly realizing that the cost of maintaining software updates and sensor calibration makes ultra-low-margin devices unsustainable. Consumers are responding favorably to this, showing a willingness to pay more for hardware that promises longevity and accuracy.

2. AI as the Next Frontier

While the Q1 2026 report highlights sensors and health-tracking, the next wave of growth is expected to come from on-device Artificial Intelligence. The ability for a wearable to process data locally—providing real-time health coaching and predictive diagnostics without relying on cloud latency—will likely be the "killer feature" for the 2026 holiday shopping season.

3. Increased Regulatory Scrutiny

As wearables move closer to medical-grade status, the regulatory environment is tightening. Companies will face increased pressure from health agencies globally to validate their data. The brands that can navigate these regulatory hurdles while maintaining their premium pricing will be the ones that define the next decade of the wearable industry.

4. Supply Chain Diversification

The 15% growth in the Chinese market, combined with the continued success of Huawei, suggests that regional supply chains are becoming more resilient. Manufacturers outside of China are expected to mirror this by diversifying their manufacturing footprints to mitigate geopolitical risks, a move that may lead to further fluctuations in production costs as the year progresses.

Conclusion

The smart wearable market has emerged from its period of stagnation, proving that the demand for integrated health and lifestyle technology remains robust. By shifting the focus toward premium hardware, industry leaders like Apple and Huawei have successfully reinvigorated consumer interest. While challenges remain—specifically regarding the declining market share of legacy players like Samsung—the overall health of the industry is strong. As we look toward the second half of 2026, the focus will undoubtedly shift from simply shipping units to providing the most sophisticated, AI-driven health insights in the palm—or rather, on the wrist—of the consumer.