The Indian Unicorn Phenomenon: A Decade of Disruption, Resilience, and Evolution

The landscape of Indian entrepreneurship has undergone a seismic shift over the last decade. Once a market dominated by traditional conglomerates and service-based IT giants, India has rapidly ascended to become the third-largest hub for startups globally. At the heart of this evolution is the "Unicorn Club"—a designation reserved for private companies valued at over $1 billion.

From the rapid-fire success of Web3 ventures like 5ire to the steady, decade-long maturation of enterprise tech stalwarts like Amagi, the journey to a billion-dollar valuation reflects the diversity and ambition of the Indian startup ecosystem. This report examines the trajectory of these high-growth entities, the capital fueling their rise, and the complex realities of their current status in an increasingly volatile global market.

1. Main Facts: The Anatomy of Indian Unicorns

The data reveals a fascinating narrative regarding the lifecycle of Indian unicorns. As of 2024-25, the ecosystem is characterized by a mix of "Active" players, those that have successfully "Listed" on public exchanges, and others navigating the "Under Valued" or "Acquired" terrain.

The Geography of Innovation

Bengaluru continues to hold the title of India’s Silicon Valley, acting as the primary headquarters for a majority of these unicorns, including giants like Flipkart, Swiggy, and Zerodha. However, the Delhi NCR region is a formidable challenger, anchoring powerhouses such as Zomato (Eternal), Delhivery, and Policybazaar. Mumbai, Chennai, Pune, and Hyderabad have also emerged as specialized hubs—Mumbai for Fintech and Media, Chennai for Enterprise Tech, and Pune for Logistics and Ecommerce.

Capital Intensity vs. Efficiency

The total funding raised by these entities varies wildly. While bootstrapped successes like Zerodha prove that sustainable growth is possible without massive dilution, others like Flipkart and Byju’s have consumed billions in capital to capture market share. The "Time Taken to Unicorn Club" metric is equally revealing; while companies like 5ire and Glance achieved the status in just one year, others, such as Billdesk, Fractal, and IndiaMart, took nearly two decades to reach the milestone, underscoring the difference between blitzscaling and long-term value creation.

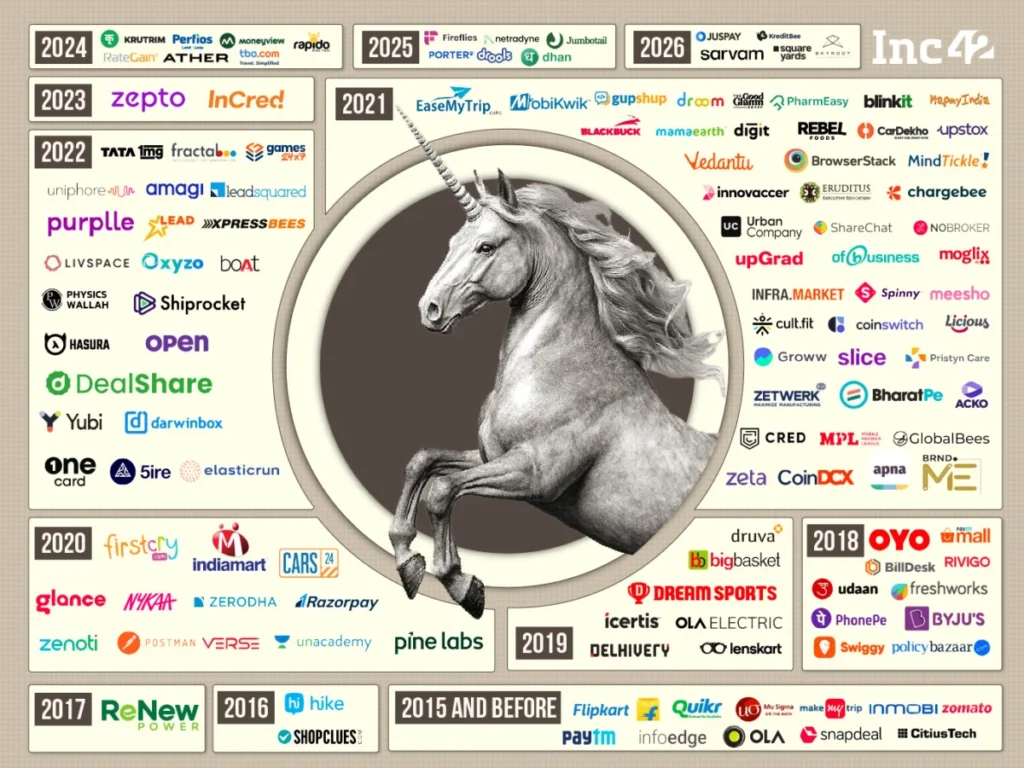

2. Chronology: The Evolution of Growth

The Indian unicorn journey did not begin simultaneously; it arrived in waves, triggered by macroeconomic shifts and digital adoption.

The Early Pioneers (Pre-2015)

The era was defined by early movers like Zoho (1996), IndiaMart (1996), and MakeMyTrip (2000). These companies laid the groundwork, proving that Indian-origin firms could scale to national and international prominence. By the time Flipkart hit its unicorn milestone in 2012, the floodgates were open.

The Acceleration Phase (2015–2020)

This period saw a dramatic shortening of the incubation period for startups. Zomato (now Eternal) achieved unicorn status in 2015, followed by a flurry of activity as mobile internet penetration in India surged. This era saw the rise of logistics and travel tech (Delhivery, Rivigo, Oyo) and the foundational growth of the Fintech sector.

The Pandemic and Post-Pandemic Boom (2021–2024)

2021 remains the defining year for Indian unicorns. During this window, companies across Web3 (CoinDCX, CoinSwitch), Fintech (CRED, Groww, Slice), and Edtech (Unacademy, Upgrad) achieved massive valuations. This period was characterized by high liquidity and global investor confidence, which has since transitioned into a more cautious, "profitability-first" environment.

3. Supporting Data: Sectoral Breakdown

The following table categorizes the primary sectors currently driving the Indian unicorn engine:

| Sector | Key Unicorns | Trends |

|---|---|---|

| Fintech | Paytm, PhonePe, Razorpay, CRED | High focus on digital payments and lending. |

| Ecommerce | Flipkart, Meesho, Lenskart, Zepto | Shift from general retail to niche and quick-commerce. |

| Enterprise Tech | Postman, Freshworks, Druva | Dominance in SaaS and cloud-based infrastructure. |

| Logistics | Delhivery, Blackbuck, Xpressbees | Critical support for the burgeoning D2C market. |

| Health Tech | 1mg, Innovaccer, Cult.fit | Rapid adoption post-pandemic. |

Note: While some companies like Byju’s and Droom are currently categorized as "Under Valued" due to market corrections, their historical impact on the ecosystem remains significant.

4. Official Perspectives and Investor Sentiment

The role of "Notable Investors" cannot be overstated. Venture Capital giants like Tiger Global, SoftBank, Peak XV (formerly Sequoia India), and Accel have acted as both financiers and strategic mentors.

Investor sentiment, however, has shifted. In interviews with industry analysts, the consensus is that the "growth at all costs" mantra is effectively dead. Investors today are prioritizing:

- Unit Economics: Can the business make a profit on each transaction?

- Path to IPO: Is there a clear roadmap for public listing, or will the company be a candidate for strategic acquisition?

- Governance: Increased scrutiny on the board of directors and financial transparency, particularly following high-profile setbacks in the Edtech sector.

Notable mentions like Zerodha stand as an outlier in this data set. By remaining bootstrapped while reaching a $3.6 billion valuation, they represent the "gold standard" for sustainable, founder-led growth in the eyes of many Indian entrepreneurs.

5. Implications: What Lies Ahead?

The Indian startup ecosystem is currently in a state of "great consolidation." The implications for the future are threefold:

A. The IPO Wave

We are seeing a transition from private equity dependency to public market accountability. Companies like Delhivery, Nykaa, Policybazaar, and more recently, Ather Energy and Swiggy, have crossed the threshold into the public markets. This trend is expected to continue as investors seek exit opportunities.

B. The Rise of Deep Tech and AI

While the initial wave of unicorns was focused on consumer internet and service-based solutions, the next generation is trending toward "Deep Tech." Startups like Sarvam AI, Ola Krutrim, and Fireflies AI represent a shift toward proprietary technology and AI-first business models, which carry higher defensive moats and global export potential.

C. The Sustainability Mandate

The "Under Valued" status of several formerly high-flying startups serves as a warning. The market is correcting for over-valuation. Future unicorns will likely take longer to reach their billion-dollar status, but they will be built on stronger foundations, higher margins, and more resilient business models.

D. Consolidation and M&A

We are seeing significant M&A activity. Acquisitions—such as Tata Digital’s entry into BigBasket and 1mg, or Zomato’s integration of Blinkit—demonstrate that the Indian ecosystem is maturing. Large platforms are absorbing niche unicorns to build "Super Apps," a strategy that consolidates market share and enhances operational synergy.

Conclusion: A Maturing Ecosystem

The Indian unicorn story is far from over. While the sheer volume of new unicorn announcements may slow compared to the 2021 peak, the quality and maturity of these companies are arguably at an all-time high. The transition from "private, high-burn startups" to "public, sustainable enterprises" is the final phase of this decade-long evolution.

For India, the goal for the next decade is no longer just to create more unicorns, but to foster companies that can compete on a global stage, generate consistent cash flows, and contribute meaningfully to the country’s GDP. The foundation has been laid; the next decade will be defined by the endurance of these businesses in the face of global economic headwinds.

Data Summary Table: Select Key Metrics

| Organization | Founded | Valuation ($ Bn) | Status |

|---|---|---|---|

| Flipkart | 2007 | 36.0 | Acquired |

| Zomato | 2008 | 30.0 | Listed |

| Blinkit | 2013 | 13.0 | Acquired |

| PhonePe | 2015 | 13.0 | Acquired |

| Swiggy | 2014 | 12.0 | Listed |

| Groww | 2016 | 11.0 | Listed |

| Info Edge | 1995 | 9.8 | Listed |

This article is based on internal market data and historical performance metrics. As the market remains dynamic, valuations and statuses are subject to change based on secondary market transactions and regulatory filings.